It actually wouldn’t add selling pressure because Opolis would need to acquire the Badger needed to process the payroll -so at most it would be neutral skewing toward net positive pressure. It also isn’t just Badger, we’re talking about the whole suite of products. If someone receives bDigg (for example) as part of their paycheck, it’s already staked and interest-bearing with exposure to bitcoin. Think about it in the real world context of my paycheck. I take 1/2 my paycheck is in cash, with the other half split between bitcoin and ETH. I’ve been doing this for nearly 1 year, and not once have I touched the ETH or BTC. I’d much rather take part of my salary in an interest-bearing badger product than vanilla pet rock bitcoin - and I sure as hell wouldn’t be selling it (and I don’t need to).

These are some neat suggestions and we are working on integrating some creative retirement solutions into our tech stack. Can’t wait to discuss this and more during the AMA tomorrow morning.

TL;DR: AGAINST. I think we could consider becoming a minor strategic investor in certain early stage opportunities where 1) there is extreme strategic alignment and 2) Badger takes a minority stake in the round alongside a proven DeFi fund.

Do we really want Badger to become a seed investment vehicle? This is a pretty big slippery slope in my opinion. We could fund hundreds of seed opportunities that seek to benefit the DeFi ecosystem in one way or another.

Regarding the specifics of the investment.

Opolis currently has an additional $1M of committed funds

$1-2M in in funds allocated from BadgerDAO

BadgerDAO will work with Opolis to fill out a round of $3-4M.

This sounds like Badger would potentially become the lead investor here. It shouldn’t be our job to lead seed-stage rounds. Badger is not a venture capital DAO. I could maybe get behind a modified BIP where Badger is a minority participant of an investment round where it is an extremely good fit to Badger’s mission of bringing Bitcoin into DeFi.

If people really want to get behind this, at least I’d propose to reduce our commitment to $1M, or even $500K, and add a provision to make our investment conditioned on the overall target being reached. I’d also feel more comfortable with Badger investing alongside a proven DeFi fund, such as Paradigm, Polychain, Parafi, Nascent, Variant, etc. Some of these are Badger investors, and I actually wonder how they would feel about this.

There is a valuation being mentioned. The proposal states 6million tokens for 2million USDC investment, from their token economics it seems that they will premine and distribute 300million tokens over the course of the first 4 years.

This means that badgerDAO will be investing in this seed-stage startup at a 100million valuation. Sorry maybe I got it wrong, but I am also alarmed at how a team member of a random startup comes out with that proposal here and the core team just votes YES without even giving an explanation of why they consider this as something that will benefit BadgerDao

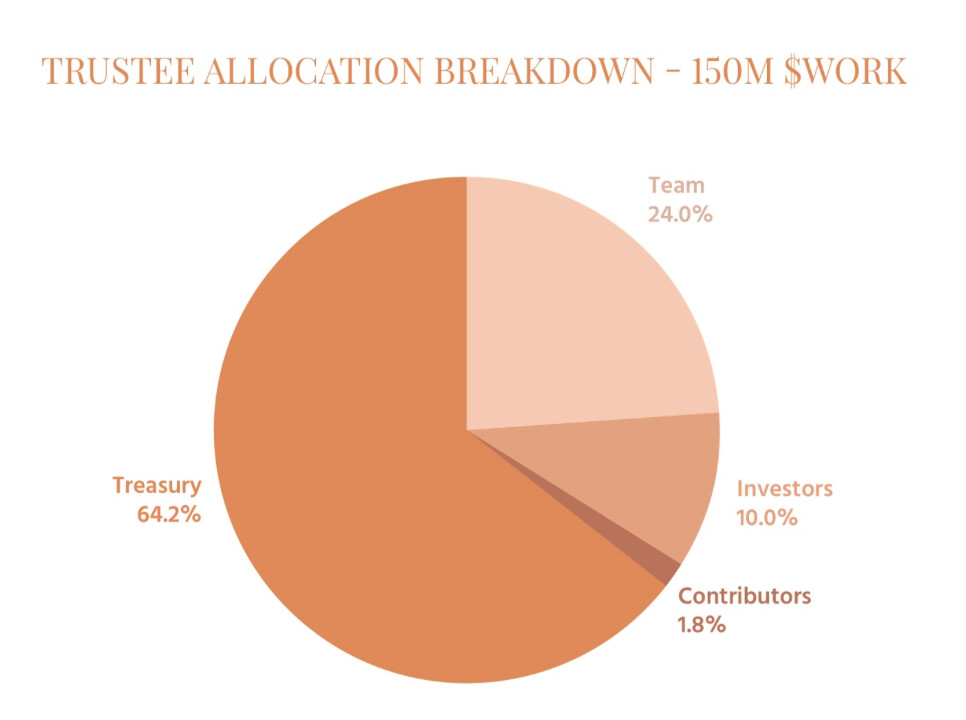

These numbers were originally released modeling 1.5M in the round. BadgerDAO would receive ~6M in the Genesis distribution from the Trustee Treasury and then hold rights to a pro-rata share of the remaining of the Trustee Treasury or ~9M. This is well above the numbers you’re suggesting. Furthermore, the supply, as you say, is locked and vested over a period of 4 years. This means the unlocked circulating supply at Genesis is less than ~30M $WORK.

Further, BadgerDAO will continue to earn more $WORK as a Coalition member for having referred its members, and other communities, to the Commons via Payroll Mining.

Thanks for everyone contributing to the discussion here. I’m siding with many of the community voices and I feel pretty strongly about this. I’m not a VC by any means but I’ve worked at/raised money w/ a number of startups.

My thoughts:

We’re not even a 6 month old startup, we should not be lead seed investors on any deal. - This deal is really bad we’re getting 1-2% of their company while leading the round. AFAIK, normal VC deals clock take up about 20% of shares outstanding (and expectation is 10x).

This seed valuation is ridiculous for an HR software company with their traction so far. This space is incredibly competitive (sure they might have an edge in the crypto space) but their TAM numbers use the full number of self employed workers in the US (most of which are non crypto). They don’t share a more realistic number of how many of that 90m is actually both independent and working in web3/crypto. That number is likely much smaller than 90m. There’s no competitive analysis of competing firms or potentially competing firms just a single statement that they have no competition (there’s a million HR firms - my guess is the reason why they aren’t targeting this segment is because this segment is small and not worth their time atm). The up and to the right growth chart is useless, they need a more realistic analysis of the market.

We should be benchmarking this deal agains other funding deals for HR software. A quick google search yields this TC article about a HR startup targeting a much larger addressable market: Humaans raises $5M seed to make it easier for companies to on-board and manage staff – TechCrunch They raised $5m (likely at a $25m valuation). There’s some noteable differences here besides their larger addressable market. If you check out their site (https://humaans.io/) they’ve already built some software that customers are onboarded to and have a strong team. They are likely further along than opolis and are raising at less than 1/4 of the valuation.

Opolis has no proof of actually already having built a complete HR software stack. My suspicion is that at this point we’re investing in an unproven team to bring together the resources to execute on their vision. There is absolutely no reason we should be investing at $80m valuation for this (if true). Normal VCs will bring in high level engineers to do due diligence and audit on the software that’s already built to see if it’s worth investing in.

VC deals are usually looking for 10-20x in 10 years. Time moves faster in the crypto space and investors look for greater multiples for the risk they’re assuming so I’d say we’re looking for 30-50x in 3-5 years. I’d need to see a convincing analysis of and roadmap for how they’re going to achieve 30-50x in 3-5 years.

My suspicion here is that in addition to the market being small. I don’t think there’s a ton of revenue to be made to offset the cost of building HR software for independent contractors (not everyone works in crypto and is flush with money - we’re also in a bull). Which is likely why there’s not a whole lot of competition in the space. But need that due diligence and analysis of how much these people are paying/willing to pay for this kind of software etc.

I think the most important thing I want to stress is that neither I nor the Badger team specializes in VC deals. We should absolutely not take this deal as a lead investor. I think we could consider a deal as a minority stake with a major crypto VC leading the round (the expectation is that a major VC should have the resources to do proper due diligence to cover gaps we’ll likely miss when doing due diligence ourselves).

Political goals from a business is a red flag. Specifically one hoping to disrupt highly regulated industries. Collective capitalism is a niche preference in the US. The risk of regulators squashing this project is way higher than your usual defi project.

If Badger gets involved in political projects regulators of one party or another may decide to come down hard on Badger DAO in retribution. Seems like a really risky path to take for a defi project. One of the advantages of defi right now is regulatory neglect.

After reviewing the proposal materials and listening to the Opolis-BadgerDAO 8x8 Meet, I am against BadgerDAO acting as the lead investor in Opolis as proposed in BIP-49. My logic is pretty simple: if the project is viable, why not co-invest alongside a credible, experienced lead investor (like one of the several funds now engaged with BadgerDAO) who can properly conduct diligence and price the round? If it’s not viable, why are we doing this?

BadgerDAO’s mission is to “bring Bitcoin to DeFi.” Not just investing, but LEADING an investment in payroll software is a deviation from this mission. If Opolis wants to offer bBadger or other assets on its platform, it should be because there is actual market demand by people to want to be paid in these tokens, not because BadgerDAO LARP’d as an angel investor in a mispriced round.

In short, if this were something that VCs (whether traditional or DeFi) were excited about and investing in, then great - let’s 1) partner with Opolis once it has proven out its MVP or 2) co-invest alongside the VCs. Plenty of upside, significantly less downside. Since there has not been any independent validation of Opolis as a compelling investment , passing this BIP implies to me is that the BadgerDAO, without any concerted due diligence or systematic pricing efforts, is better able to see the value of a payroll software product than those who spend 100% of their time and effort looking at these sorts of projects.

I also agree that this is an incredibly thoughtful and well-written BIP. Opolis seems like a fantastic firm and no doubt will be successful.

I also concur with @shakeshack that I don’t think we’re the right fit for this specific position at this point in time. Just because we can, doesn’t mean we should.

As a DAO whose self-stated purpose is to ‘bring bitcoin to defi,’ to have the DAO commit funds to this BIP feels well reasonably outside our core mission. Were the DAO several more months/a year into maturity, I would say this would be more worth entertaining.

I would welcome a tight collaboration in the future, but this doesn’t strike me as mission critical nor overwhelmingly beneficial for both sides.

Same. changed mine as well from a yes to a NO. Let’s get refocused on building $BADGER and stop acting like an angel investor. Yes we can do this with our treasury funds - doesn’t mean it’s the best thing for us right now.

A question: What will happen when someone wants to be paid in ETH, what with the high gas fees? Will Opolis eat the costs of transferring ETH to workers, decreasing Opolis’s revenue, or will the worker get the cost taken out of their pay, decreasing their paycheck total? Neither seems like a good outcome. And as the price of ETH increases, gas will increase…

Another question: You say that Opolis will get their revenue from the 1% fee they charge. That’s all well and good, but cryptos fluctuate enormously, sometimes 10% or more in a single day. What’s the time window for Opolis holding funds? If it’s more than a day, if they buy say 10 BTC to pay workers, and there’s a big drop in the price of BTC, there’s the potential for Opolis to lose a lot of money, maybe more than they can handle. After all, they’d need to buy even more BTC in the above scenario, in order to pay the workers an amount equal to their pay. It would be better if they keep the time window at less than a day, to avoid this scenario. Will they?